European Commission introduced new support mechanism for the ramping up of Sustainable Aviation Fuels (SAF) deployment

Sustainable Aviation Fuels (SAF) are renewable fuels that replace fossil based kerosine in aircrafts and are seen as an important option to mitigate climate emissions in the aviation sector. Generally, these alternative fuels are more expensive than their fossil counterpart, kerosene. In order to support the uptake of SAF, the European Commission has introduced several policy instruments.

As part of the ‘Fit-for-55’ package, the European Commission introduced the ReFuelEU Aviation measure, which promotes increased used of SAF. This mandates fuel suppliers to gradually increase the share of SAF supplied to EU airports. In addition, aviation is included in the scope of the EU Emission Trading System (EU ETS), which applies to intra-EU flights. The ‘cap-and-trade’ system applies a price related to emissions arising from the use of fossil fuels on board aircrafts.

In the 2030 revision of the ETS directive, the European Commission introduced a support mechanism involving the setting aside of ‘SAF allowances’. These allowances will be used to bridge the price gap for the use of alternative fuels to accelerate the roll out of SAF.

We have reviewed this mechanism in order to assess its expected impact on bridging the price gap and boosting volumes of SAF delivered to the market. After reviewing the EU ETS support mechanism for SAF, we conclude that the policy design is insufficient to support the broader development of the SAF market.

We summarise our full assessment of the mechanism below:

- The support mechanism only provides limited short-term support on the demand-side and does not offer long-term investment security for SAF producers.

- The design of the policy instrument does not establish a level playing field for the alternative aviation fuel options: limiting the competitive pricing environment.

- The support instrument is high-cost relative to its emission saving potential, compared to potential savings achieved through awarding support to producers.

Core principle of the ETS allowances for SAF mechanism is to reduce the price gap

On 6 February 2025, the European commission adopted the rules for the financial support mechanism for the uptake of SAF under the EU ETS[1] (see notes at the end of the blog). This involves reserving 20 million allowances, which will be allocated to aircraft operators, who report the use of eligible sustainable aviation fuels. These allowances have a value equivalent to approximately €1.5 billion[2]. The allowances will be awarded to eligible aircraft operators (in scope of EU ETS) who report and demonstrate the use of eligible aviation fuels during the period 2024-2030.

The level of support will be determined by the price gap between the average fossil kerosene price each year (as well as considering the ETS price and difference between harmonised level of taxation on fossil kerosene and SAF). This will be based on average annual prices to be reported by the European Commission, on the basis of the European Aviation Safety Agency (EASA) technical report. Where market price data is not available, aircraft operators may report actual prices paid (if supported with sufficient documentation). Or a conservative 10% margin may be applied by the European Commission to production cost estimates provided by EASA to establish a minimum market selling price.

The SAF allowances can be awarded for the use of fuels which are eligible under ReFuelEU aviation which do not stem from fossil fuels. The final level of financial support depends both on the category of fuel and specific attributes of the aircraft operator. Some examples are outlined below[3]:

- For bio-SAF:

- 50%: Aviation biofuels (produced from feedstock listed in Annex IX-B) – in this analysis we use the term SAF (IX-B),

- 70%: Advanced aviation biofuels (produced from feedstock listed in Annex IX-A), or SAF (IX-A),

- 95%: Synthetic Aviation Fuels (RFNBO: Renewable fuels of Non-Biological Origin), or in this report stated as e-SAF

Assessing the new price gap reveals an unlevel playing field for SAF options

We present an analysis to show the impact of the financial support mechanism on the price gap between fossil kerosene and eligible SAFs. This is based on reference prices provided in the EASA (2024) market report on SAF[4] for prices in 2023.

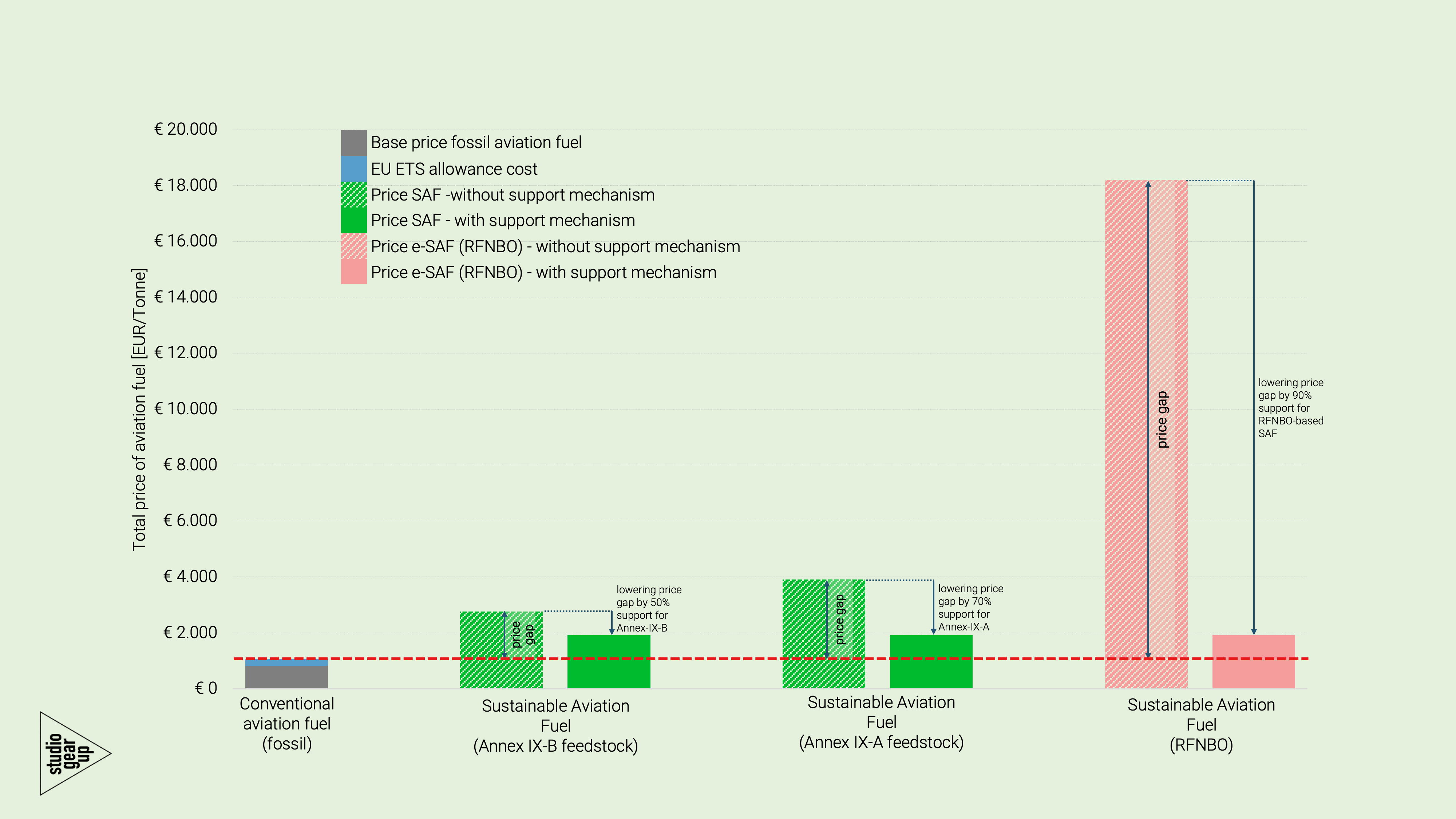

Figure displays the expected impact of the EU ETS support mechanism on the price gap between conventional (fossil-based) aviation fuel with synthetic aviation fuels (RFNBO), advanced aviation biofuel (Annex IX-A feedstock category), and aviation biofuels (Annex IX-B feedstock category).

While the financial support mechanism offers a significant reduction in the current price gap, it does not entirely bridge the price difference. As shown in Figure 1, the 50% financial support awarded to SAF (Annex IX-B) would lower the existing price gap from approximately 1,715 €/tonne fuel to 858 €/tonne fuel. In addition, the 70% financial support awarded to SAF (Annex IX-A) could lower the existing price gap from approximately 1,890 €/tonne to 567 €/tonne. Finally, the 95% support allocated to eligible e-SAF could reduce the existing price gap to the price of conventional fossil fuel (including the EU ETS allowance price) from approximately 7,197 €/tonne to 360 €/tonne, resulting in the lowest price gap of the three considered SAF options.

This demonstrates that the support awarded does not establish equal pricing conditions for the different aviation fuel options. The mechanism offers higher levels of financial support to synthetic and advanced aviation fuels, leaving space for these producers of these fuels to maintain higher market prices while maintaining a competitive pricing position. In our assessment the price of e-SAF could be as high as 18,210 €/tonne and the price of a SAF (Annex IX-A) as high as 3,912 €/tonne, while maintaining a competitive pricing position (after application of the support mechanism with SAF (Annex IX-B), see Figure 2. This ultimately may limit the incentive for synthetic and advanced aviation fuel producers to deliver to the market at lower prices and may not support the development of a competitive pricing environment for alternative aviation fuels.

The outreach of the support mechanism is limited in the context of ReFuelEU Aviation

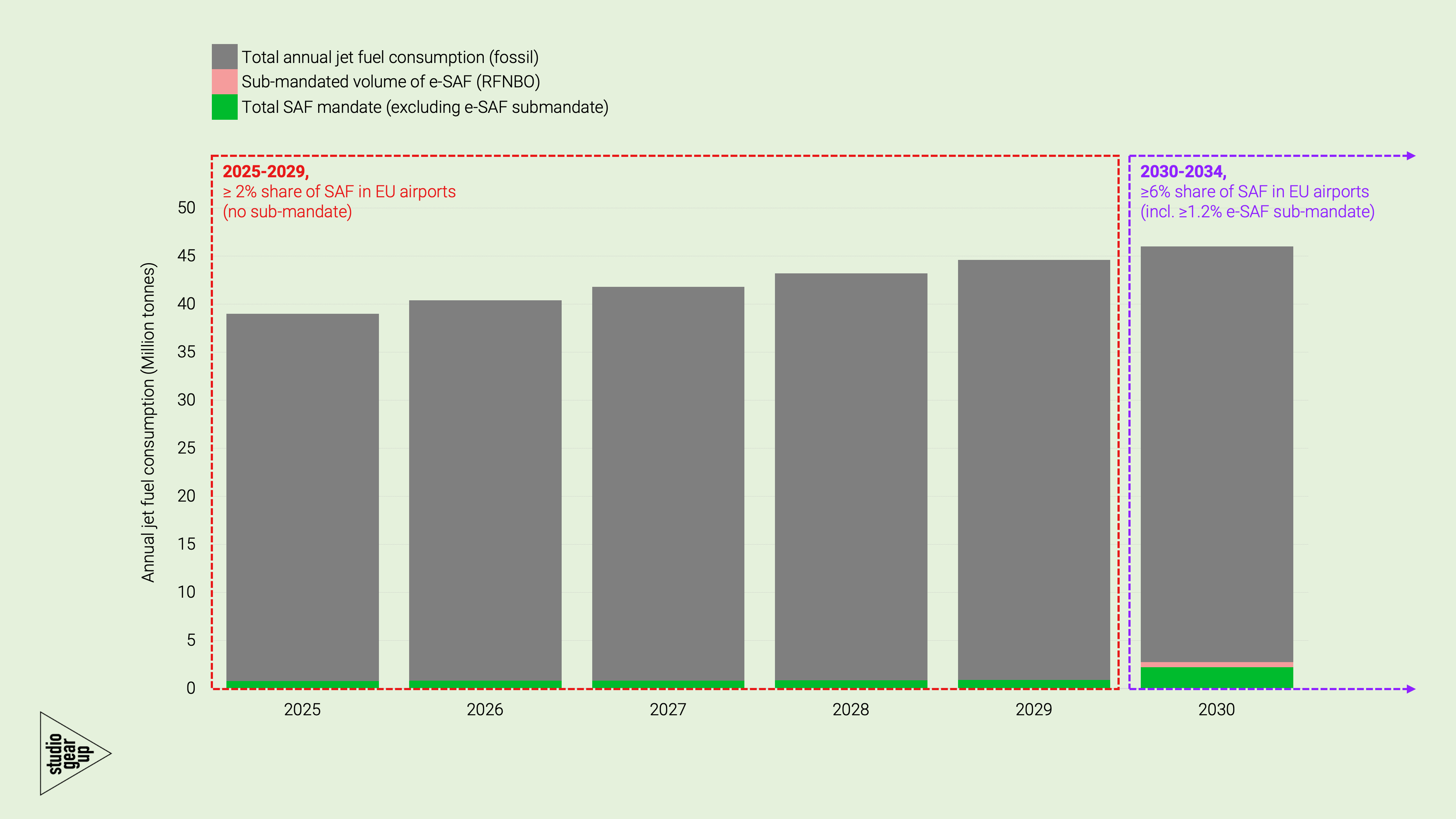

To offer a perspective on the quantity of fuels that this support mechanism could be applied to, we evaluate the proportion mandated renewable fuels under ReFuelEU Aviation which may be eligible to receive financial support. Given that the support mechanism will only be awarded for flights within the scope of EU ETS (intra-EU aviation), a proportion of fuels mandated by ReFuelEU Aviation could be excluded from receiving this financial support. Specifically, SAF used on flights from EU airports to regions outside of the EU. However, we expect most SAF volumes will be used for domestic travel, given the incentive for using SAF for domestic aviation purposes: to avoid ETS costs and receive free allocation.

Figure 3 shows the expected development of jet fuel consumption in the EU and the minimum share of SAF mandated by ReFuelEU Aviation. The share of SAF required under ReFuelEU Aviation is a 2% minimum share between 2025-2029 and a 6% minimum share in 2030. In 2030, a sub-mandate requiring a minimum share of 1.2% synthetic aviation fuel is also applied. Based on expected developments in the jet fuel consumption across the EU, the minimum volume of SAF which must be delivered to the market during the period 2025-2030 is approximately 6.4 million tonnes. With an additional 0.6 million tonnes sub-mandate of synthetic aviation fuels required in 2030.

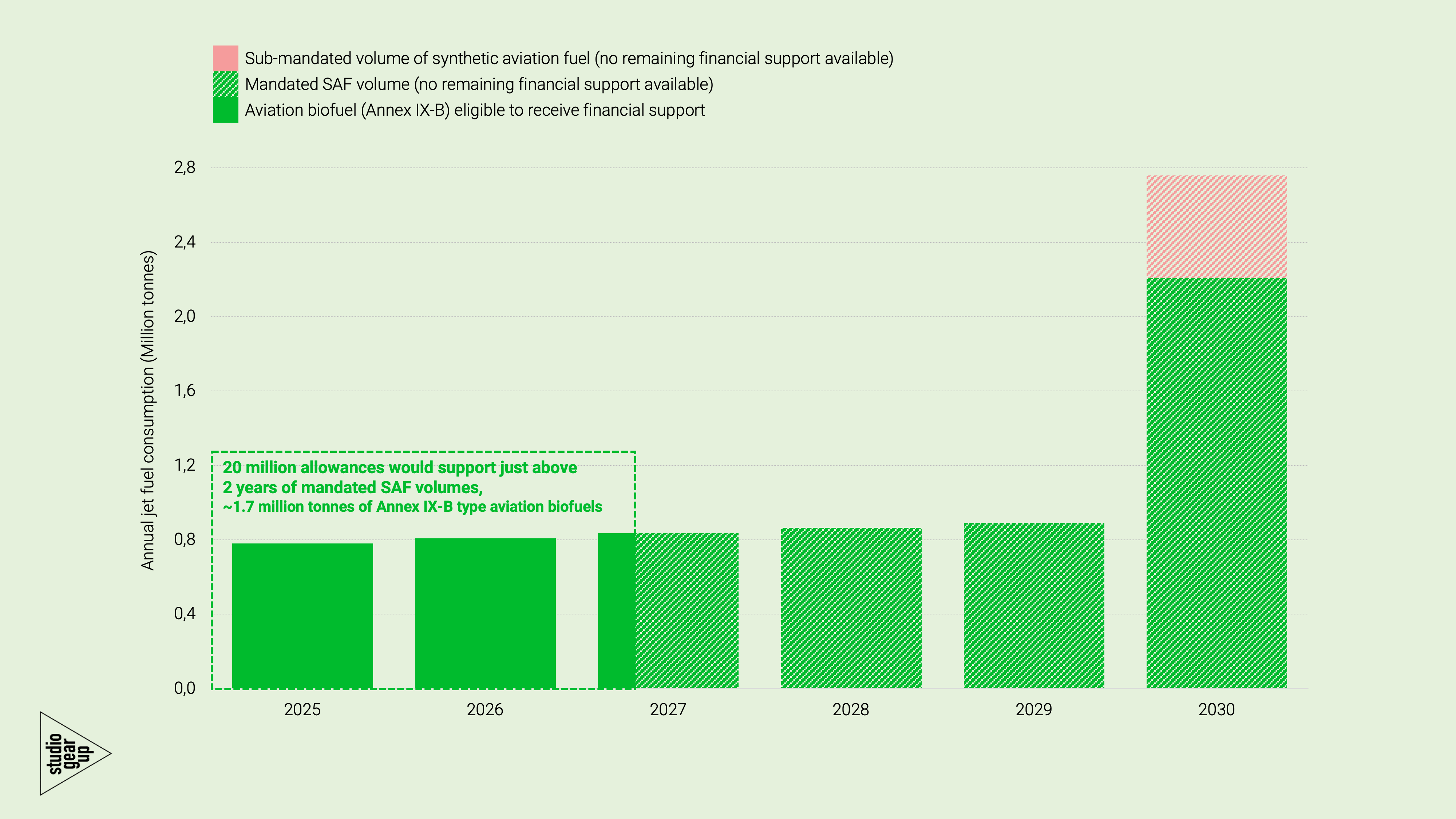

We explored the scenario in which the financial support mechanism is entirely allocated to SAF (Annex IX-B). SAF (Annex IX-B) is currently the most commercially available SAF option on the market (for example, HEFA). While there are quite a number of SAF projects are announced for bioSAF based on Annex IX-A or e-SAF (RFNBO), these are still largely in the planning phase. Our assessment reveals that, in the context of the fuel mandates under ReFuelEU Aviation, the EU ETS aviation mechanism offers limited support. Providing 50% price gap support to SAF (Annex IX-B0 would support about approx. 1/4th of the total mandated SAF volume to be deployed in the 2025-2030-time frame.

Based on the expected value of the reserved 20 million allowances and the level of financial support awarded to SAF (Annex IX-B) – 50% of the price gap – we estimate that approximately 1.7 million tonnes of aviation biofuels could be eligible to receive financial support. Being fully supported as of the beginning of the year 2025 the SAF allowance budget would be depleted in the first quarter of 2027, allowing for no support to e-SAF (assuming eSAF enters the market at the moment of the sub mandate introduction in 2030) See Figure 4.

High-cost policy instrument relative to potential GHG emission savings, direct investment into SAF production may offer a better path to achieving emissions saving

The mechanism awards 20 million allowances of total support, which is equivalent to the value of approximately € 1.5 billion. This represents a cost to the European Commission, in the form of forgone EU ETS revenue for the sale of allowances. Following our assessment above, we explore the scenario in which the price mechanism supports the delivery of 1.7 million tonnes of SAF (Annex IX-B) to the market. This is equivalent to ~5.5 million tonnes of GHG emission savings from the avoided use of fossil kerosene.[5] Assuming that the mechanism delivers this volume of fuel to the market, this would represent a total abatement cost of 273 €/tonne GHG emissions.

In terms of emission saving potential, this can be considered as the most optimistic scenario. The higher cost required to bridge the price gap for advanced and synthetic aviation fuels will demand greater quantities of allowances to achieve the same quantity of avoided emissions (from replacing fossil kerosene with sustainable alternatives). For the purpose of this analysis, we have assumed that no volumes of SAF (Annex IX-A) or e-SAF are delivered to the market. However, in reality, we expect that in the coming years these fuels will be delivered to the aviation sector in some capacity. Therefore, our assessment represents an “upper level” of emissions savings based on the current price gap between fossil kerosene and alternative aviation fuels.

We explore an example of a recent grant awarded under the EU Innovation Fund, a grant platform entirely funded by EU ETS revenue, to compare the expected impact of the support mechanism against providing direct financial support to SAF production facilities.

In December 2023, the Biorefinery Ostrand was awarded 167 million euro in grant from the Innovation Fund: a Swedish producer of advanced biofuels and electro-fuels, expected to start operation in 2029[6]. This will be the first commercial scale biorefinery producing SAF and naphtha from solid forest residues, via gasification and FT synthesis. As shown in the project factsheet published by the European Commission, this project is estimated to achieve an accumulated 8.7 million tonne in GHG emissions avoidance during the first ten years of operation. That is equivalent to twice the total annual emissions from domestic aviation in Sweden.

To put this into context, the 167 million euro investment of direct support awarded from the EU Innovation Fund is expected to support the development of a project achieving 58% higher emission savings than that of the SAF support mechanism. At a cost of € 1.5 billion for the support mechanism, around 9 times higher than the grant awarded by the innovation fund, this suggests direct investment into production facilities provides better long-term support for emissions saving.

Additional support mechanisms are required targeting SAF producers

Our recommendation is that the Commission considers alternative support mechanisms which provide security for renewable fuel producers. These must offer upfront financial security for producers and encourage investment into new production facilities[7].

This should involve the targeted use of ETS revenues to support SAF production projects and compensate the price gap. Taking advantage of the financial instruments available under the Innovation Fund, “Competitive Bidding” auctions. Specifically, we recommend using the double-sided auction mechanism to efficiently determine the allocation of financial support and award support on both the demand- and supply-side, awarding long-term support and investment security for SAF producers.

Conclusion: long-term supply-side measures are still required to support SAF production

The new EU ETS aviation support mechanism aims to support the roll out of Sustainable Aviation Fuel (SAF) in the coming years. While this mechanism will be appreciated by aircraft operators, this is a short-term demand-side policy instrument which does not provide long-term investment security for SAF producers. Additional measures must be implemented at a broader scale, designed to support long-term supply-side investment security for SAF producers. Specifically, we recommend using revenue obtained from the sale of EU ETS allowances via a double-sided auction mechanism.

Notes

[1] For more information on the adoption of EU rules on the ETS support system to accelerate the use of SAF see the Delegated Regulation C(2025)681 and its Annex document on laying down detailed rules for the yearly calculation of price differences between eligible aviation fuels and fossil kerosene and for the EU ETS allocation of allowances for the use of eligible aviation fuels at: https://climate.ec.europa.eu/news-your-voice/news/adoption-eu-rules-ets-support-system-accelerate-use-sustainable-aviation-fuels-2025-02-06_en

[2] Based on an assumed average EU ETS allowance price of 75 €/tonne. This price is used throughout this article.

[3] Further details can be found in the Annex of the Regulation. In the annex Document more eligible aviation fuel subcategories are presented, but in this analysis, we have focused on bio-SAF (Annex IX-A and Annex IX-B) and e-SAF (RFNBO).

[4] See https://www.easa.europa.eu/en/document-library/general-publications/state-eu-saf-market-2023

[5] Based on the emission factor stated in EU ETS Directive, Annex III (Table 1), value for jet kerosene (Jet A1 or Jet A)

[6] See https://ec.europa.eu/assets/cinea/project_fiches/innovation_fund/101132801.pdf

[7] We support the call for policy interventions for the aviation industry by Project SkyPower, who wrote an open letter to the Commission (17, February 2025), calling for policy interventions to unlock the scale up of e-SAF in the EU.